Why a Mid-Year Insurance Review Matters for Texas Families

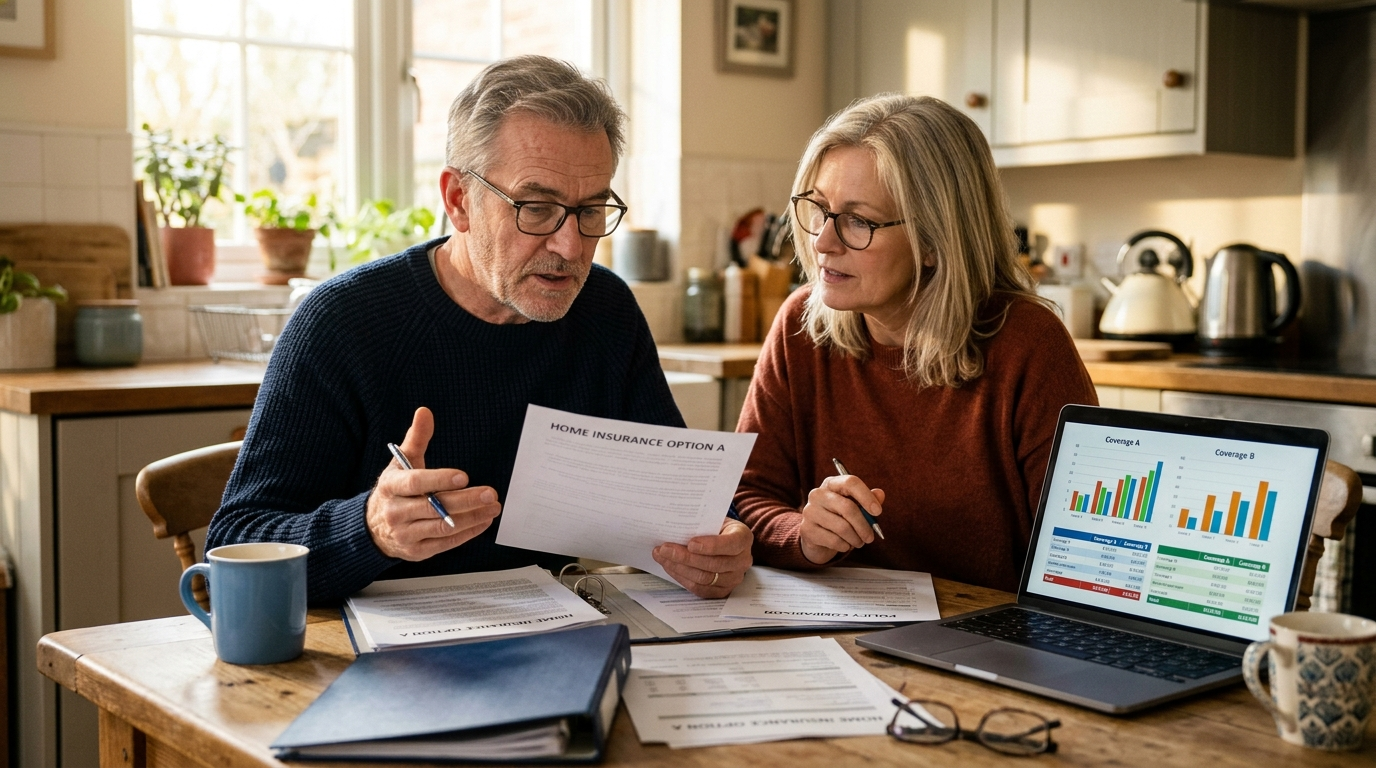

We are halfway through 2026, and if your insurance policies have been sitting in a drawer since you last renewed them, now is the perfect time for a mid-year insurance review. A lot can change in six months, and here on the Gulf Coast, the second half of the year brings the heart of hurricane and severe-weather season. Taking an hour now to look over your coverage can save you money, close dangerous gaps, and give you real peace of mind heading into the riskiest stretch of the calendar.

At JAMCO Insurance in Pasadena, we sit down with Houston-area families all the time who assume their policies still match their lives. More often than not, something has shifted, a new car, a teen who started driving, a kitchen remodel, or simply a renewal that quietly raised a deductible. A mid-year insurance review is your chance to catch those changes before they turn into an unpleasant surprise at claim time. Think of it the way you would a doctor's checkup: a quick look while everything is calm beats an emergency later.

Start With Your Home Insurance

For most Texas families, the home is the single largest thing they insure, so it is the right place to begin. Pull out your homeowners declarations page and look closely at your dwelling coverage, the amount that would rebuild your house from the ground up. With construction and labor costs in the Houston metro still elevated, a policy written even two or three years ago may no longer cover the true cost to rebuild. If a storm took your home down to the studs, you want enough coverage to put it back exactly as it was.

Pay special attention to your wind and hail deductible. Along the Gulf Coast, many policies carry a separate percentage-based deductible for named storms, often one or two percent of the dwelling value rather than a flat dollar amount. On a 350,000 home, a two percent wind deductible is 7,000 out of pocket before coverage kicks in. Knowing that number now, rather than after a hurricane, lets you plan an emergency fund or talk to us about adjusting it.

Coverage Gaps Texas Homeowners Often Miss

- Flood insurance — Standard homeowners policies do not cover rising water. In our flood-prone region, a separate flood policy is essential, and there is typically a 30-day waiting period, so do not wait until a storm is in the Gulf.

- Personal property limits — If you bought new furniture, electronics, or jewelry, your contents coverage may need a bump or a scheduled rider.

- Replacement cost vs. actual cash value — Replacement cost pays to buy new; actual cash value subtracts depreciation. Know which one you have.

- Loss of use — This covers hotel and living expenses if your home is uninhabitable after a covered loss, something that matters a great deal during a regional disaster.

If any of this raises a question mark, it is worth a closer look at your homeowners insurance coverage with an agent who knows the local risks. Small adjustments today can make an enormous difference when you actually need to file a claim.

Review Your Auto Insurance and Look for Savings

Auto insurance is the second pillar of your mid-year insurance review, and it is often where families find the quickest savings. Texas roads, and Houston traffic in particular, mean your auto policy works hard, but it can also drift out of step with your life. Start by confirming the vehicles listed are the ones you actually own, and that the drivers on the policy reflect your current household. An outdated policy can mean you are paying for a car you sold or, worse, that a regular driver is not properly covered.

Next, look at your liability limits. Texas requires only minimum coverage, but those minimums can be dangerously low if you cause a serious accident. Bumping up liability is usually surprisingly affordable and protects your savings and home from a lawsuit. While you are at it, review whether you carry uninsured and underinsured motorist coverage. With many drivers on the road carrying only the bare minimum, or no insurance at all, this protection is one of the smartest dollars you can spend in Texas.

Discounts You May Be Leaving on the Table

Insurance carriers offer a long list of discounts that families forget to claim. As part of your review, ask whether you qualify for any of these:

- Bundling — Combining home and auto with one carrier often unlocks the biggest single discount available.

- Safe driver and telematics — A clean record, or a usage-based program, can meaningfully lower your premium.

- Good student — Teen and college drivers with strong grades frequently earn a break.

- Vehicle safety features — Anti-theft devices and modern safety tech can reduce what you pay.

- Paid-in-full and paperless — Small administrative discounts that add up over a year.

If you have never compared your rate against other carriers, the middle of the year is a great moment to do it. Take a look at how you can compare car insurance rates and save, or explore the savings that come from choosing to bundle your home and auto insurance under one roof. As an independent agency, we can shop multiple companies on your behalf instead of being locked into a single one.

Re-Examine Your Deductibles and Out-of-Pocket Risk

Your deductible is the amount you pay before your insurance contributes, and it directly shapes both your premium and your financial exposure. A higher deductible lowers your monthly cost but means more out of pocket when you file a claim. A lower deductible costs more month to month but cushions you at claim time. The right balance depends on your emergency savings and your comfort with risk, which is exactly why a mid-year insurance review is the moment to revisit it.

For Gulf Coast families especially, the wind and hail deductible deserves a second look. Run the math on what you would actually owe after a major storm and ask yourself honestly whether you could write that check tomorrow. If the answer makes you uneasy, we can model a few different deductible scenarios so you can see the trade-off between premium and protection in plain dollars. There is no single right answer, only the one that fits your family's finances.

Account for Life Changes Since Your Last Review

Insurance is meant to follow your life, and life rarely stands still. The most common reason coverage falls out of alignment is a major change that never got reported to the carrier. As you work through your mid-year insurance review, walk through the past six to twelve months and ask whether any of these apply to your household.

- You got married or divorced — Combining or separating households changes who and what needs coverage, and may open new discount opportunities.

- You welcomed a new baby — A growing family is the classic prompt to review life insurance and make sure your loved ones are protected.

- You bought a new car — A new vehicle should be added promptly, and you will want to confirm gap coverage if you financed it.

- You renovated your home — A new kitchen, an added room, or a finished garage raises your rebuild cost and should be reflected in your dwelling coverage.

- You have a new teen driver — Adding a young driver is a significant change; reviewing limits, discounts, and which car they drive can manage both risk and cost.

- You started a side business or work from home — Home-based business equipment and liability often need coverage your homeowners policy will not provide.

Each of these milestones is a moment where the right coverage adjustment protects you and the wrong assumption leaves you exposed. If you have experienced any of them and have not updated your policies, put that at the top of your checklist.

How JAMCO Insurance Makes Your Mid-Year Review Easy

Going through every policy on your own can feel overwhelming, and that is where having a trusted local agent in your corner makes all the difference. As an independent insurance agency serving Texas, JAMCO Insurance is not tied to one company. We represent many carriers, which means we can compare your options side by side, hunt down every discount you qualify for, and tailor coverage to the specific risks of living on the Gulf Coast. We do the legwork; you get clarity and confidence.

The best part is that a mid-year insurance review costs you nothing but a little time, and it could save you real money while closing gaps you did not know you had. Before hurricane season ramps up, let our Pasadena team take a fresh look at your home, auto, and overall protection. You can schedule a free policy review with us today, or reach out through our contact page for a free quote. Prefer to talk it through? Call JAMCO Insurance at (832) 777-5260 and we will walk you through your checkup step by step. A quick review now means a calmer, better-protected second half of the year for your family.

Get A Quote

At JAMCO, securing your future is easy. Ready to protect what matters? Contact us for a quick quote and personalized insurance options!

Kelly

Speak to Kelly 24/7

Microphone ready

Start your custom insurance quote

Instant answers to your insurance questions

Schedule appointments or follow-ups

Personal Insurance

From auto and homeowners to renters and umbrella policies, we help protect your family and property. Let’s find coverage that fits your life.

Commercial Insurance

We customize policies for your industry's risks, like general liability and workers' comp, ensuring you can run your business worry-free.

Contact JAMCO Insurance

Recent Posts